MA Withholding Requirement on Sale of Real Estate by Nonresidents

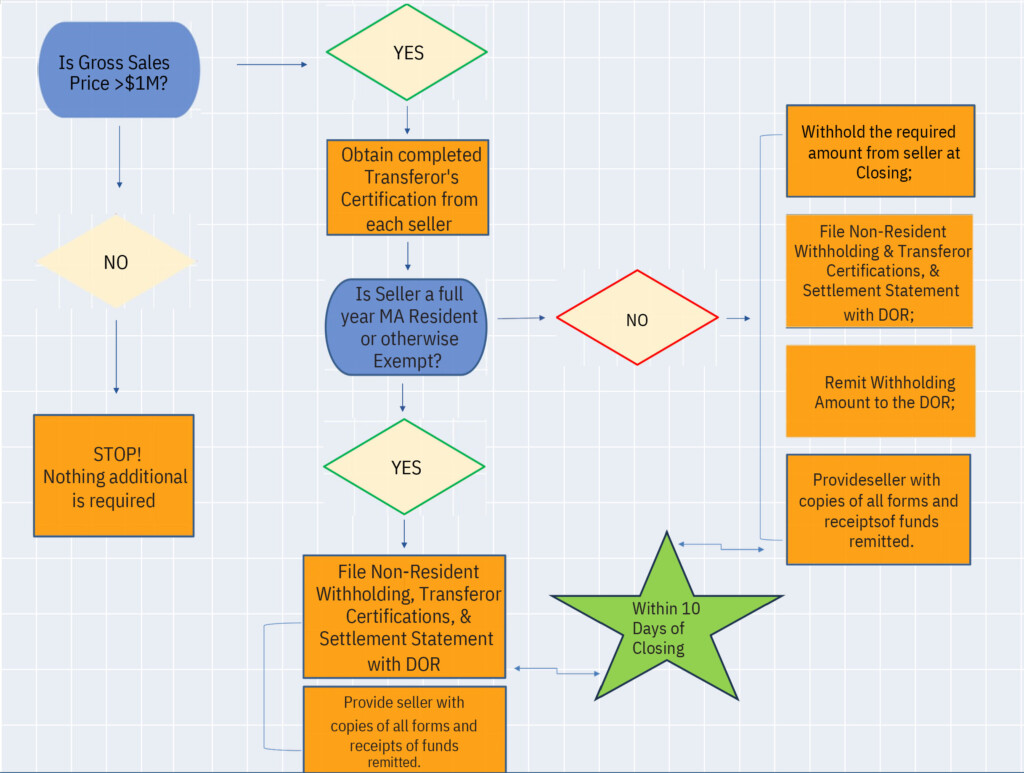

The new MA withholding requirement, regulation, 830 CMR 62B.2.4, went into effect on August 15, 2025 and it applies to real estate closings that occur on or after November 1, 2025. The withholding applies to property sales with a gross sales price of $1,000,000 or above where the seller is a non-resident individual, part-year resident, or a corporation that does not maintain a place of business or is not registered with a Secretary of State to do business in MA. The measure is intended to ensure the collection of state income and corporate excise tax from the sellers who may not otherwise file taxes in Massachusetts. The closing attorney, the escrow agent or the title company will act as a withholding agent and will handle the tax withholding. Each seller going forward will be required to fill out a Transferor’s Certification even if they are exempt from the withholding and give it to the withholding agent on or before the closing. The withholding agent will use the information provided on the Transferor’s Certification to complete and file the Form NRW: Nonresident Real Estate Withholding. The withholding agent must remit the withheld tax to DOR within 10 calendar days of closing. The standard withholding rate is 4% of the gross sales price. If the seller’s capital gains are over $1 million dollars (for 2025 it is $1,083,150 and it is an annually inflation-adjusted threshold), then they will be subject to an additional 4% surtax to cover the millionaire’s tax. If a non-resident seller elects to base the withholding on their estimated net gain, then the rate is 5%. The tax rate amount on taxpayers subject to the corporate excise is 4% of the gross sales price. If the seller elects to use the alternative withholding calculation, the tax rate will be 8% of the estimated net gain.

After filing of the NRW form, the withholding agent will provide a statement to the seller. In addition, DOR will issue a Massachusetts Nonresident Real Estate Withholding Statement to the seller that had withholding tax paid on their behalf in the prior calendar year. The statement will be sent by end of January in the year following the closing date. The seller will need this information when claiming the withholding on their MA return, similar to a form W-2 or a 1099. Feel free to consult your attorney and refer to mass.gov for additional details.

For the withholding agent:

Here’s a summary of the applicable rates:

For personal income tax sellers (non‐resident individuals):

Standard method (gross sale price) → 4%

Alternative method (net gain) → 5%

For corporate excise tax sellers (nonresident corporations without MA business presence):

Standard method (gross sale price) → 4%

Alternative method (net gain) → 8%

Who is exempt from the withholding?

The following types of sellers will be exempt from the withholding requirements, but only if they provide a Transferor’s Certification:

• Full-year Massachusetts residents

• Pass-through entities

• Publicly traded partnerships

• Estates of resident decedents

• Resident trusts

• Corporations with a continuing Massachusetts business presence

• Organizations qualified under Internal Revenue Code (Code) § 501(c)(3), unless the sale/transfer results in unrelated business taxable income

• Insurance companies

• The U.S. government, Massachusetts, or any political subdivision, or their respective agencies

• The Federal National Mortgage Association, the Federal Home Loan Mortgage Corporation, the Government National Mortgage Association, or a private mortgage insurance company

• Financial institutions

• Certain real estate investment trusts

![]()

Let’s walk through a simple numerical example of how Massachusetts non-resident withholding works on a sale:

Example:

• Seller: Non-resident individual (legal residence is in NY)

• Property: Condo on Nantucket, MA

• Sale price: $1,200,000

• Original purchase price (cost basis): $900,000. Assume that no improvements have been made.

• Selling expenses: $80,000 (broker compensation, legal fees, etc)

• Closing date: After November 1, 2025

• Withholding tax rate (standard): 4% of gross sale price if gain is unknown

• OR 5% of the estimated net gain if seller elects alternative calculation and documents it.

Scenario 1: Gain Unknown at Closing

If the gain is not calculated/documented by closing, the withholding is 4% of the gross sale price:

4%×$1,200,000=$48,000

Withholding amount: $48,000

The seller can later file a MA non-resident income tax return (Form 1-NR/PY) to reconcile the actual tax due and potentially receive a refund if too much was withheld.

Scenario 2: Gain Known and Alternative Method Elected

If the gain is calculated and the seller elects the alternative method (5% of gain):

Calculate gain:$1,200,000−$900,000−$80,000=$220,000

Withhold 5% of gain: 5%×$220,000=$11,000

Withholding amount: $11,000

This approach usually results in a smaller upfront withholding, but it requires proper documentation at closing. Most sellers will try to document their estimated gain before closing to use the alternative method as it will significantly reduce the amount withheld.

All parties involved in a real estate transaction in MA should take time to familiarize themselves with this new regulation. Feel free to refer to a set of frequently asked questions and answers related to this new tax obligation published by the state. I am also happy to connect you with a trusted local attorney who can be of further assistance regarding this regulation.

Looking for more real estate updates and Nantucket resources? Visit the Fisher Real Estate blog for market insights, guides, and community news.