![]()

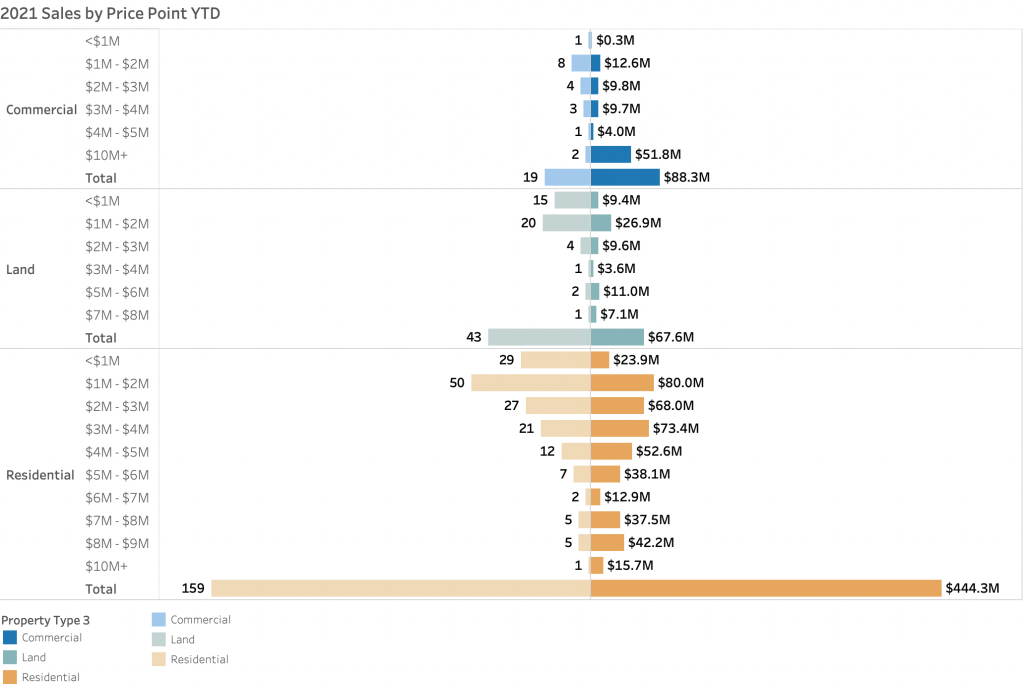

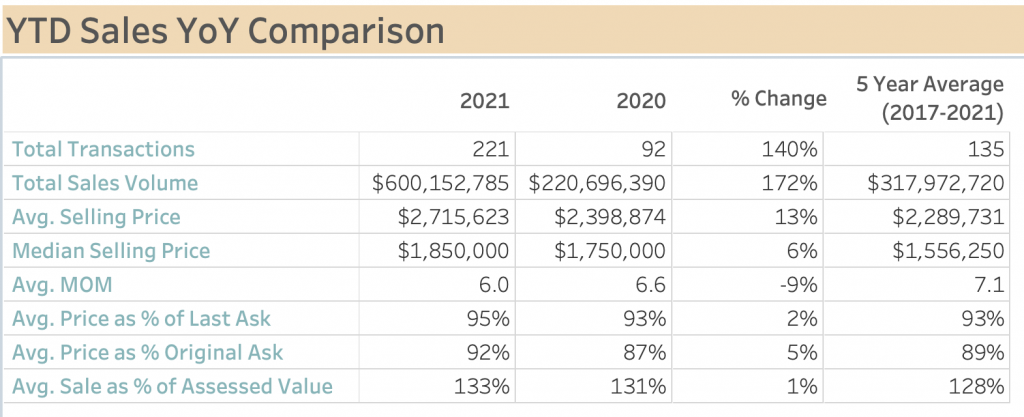

Just when we thought historic records couldn’t possibly continue to be dwarfed, we saw the preliminary sales data for April. And though we are still culling through the records to scrub the data, initial results show that April 2021 sales included 70 transactions totaling $250 million. That’s right, $250 million in sales in the month of April alone. Since 2005, the average dollar volume witnessed in April is typically only $47 million. April 2021 saw five times the volume of the historical average. This brings total Nantucket real estate sales to 221 transactions totaling $600 million through April 30, 2021. This is a 140 percent and 172 percent increase from 2020, which happened to be a record year for the island.

To be fair, approximately $64 million of this volume was from commercial real estate transactions, including over $50 million that resulted from the acquisition of several B&B related businesses in town (some of which traded just a few years ago but were recapitalized by a different investment group). Yet, even if you strip these sales from the total, the numbers are more than impressive. Here are a few notable points we’ve gleaned from our initial review of the data:

• High-end sales above $5 million resulted in $90 million of this total.

• The highest price per square foot paid in April was $2,800 for a waterfront property in the Squam area. The next highest was $2,650 per square foot for an Old North Wharf property. There were several others above $2,000 per square foot without a water component.

• Two properties sold for more than the last asking price while 20 others sold for full asking price (this number is approximate due to off market listings being added post-closing into the MLS).

• Both the commercial real estate sector and pre-construction lot sales continued to show solid momentum.

• There were several re-trades that showed surprisingly modest appreciation, anywhere from zero to four percent. This comes with the caveat that most of these were development properties when they first sold (meaning buyers paid a premium for new construction). As evidenced by historic data, very little appreciation typically occurs in the first few years of ownership.

The good news (for buyers) is that substantially more inventory came to market in April during the last few months, signaling we may continue to see more properties come to market as we move into the warmer months. The not so good news for buyers is that the number of properties going into contract quickly was also quite high. Both new contracts and closed sales during the month of April kept continued pressure on inventory and propelled property values.

With nearly 70 properties (also a record) going into contract in April, the market is not showing signs of slowing down. Stay tuned for our more in-depth analysis of April sales data in our monthly report in the coming weeks.